Focus on being debt free, generating passive income or growing net worth?

It has been a relaxing few days as i took leave to focus on my personal finance and plan for myself how to continue my pursuit for financial freedom in 2014. I read with huge interest some bloggers who attain passive income of more than $1,000 a month this year and another blogger who became debt free at a relatively young age by paying off their HDB mortgage loans in its entirety.

A very mind intriguing thought came to my mind. In our pursuit for financial freedom, do we want to focus on Net Worth, focus on Cash Flow or focus on being Debt Free? There is no right or wrong answer but the mindset can lead to very different outcome eventually and a lot will depend on which stage of the life cycle we are currently in. Let me give you a simple illustration.

Illustration

Assuming a young couple in their early 30s managed to save $100,000 and this year, they received a bonus of $100,000. With $200,000 in the bank earning low interest, they were wondering what to do with the money. They currently have 2 kids and a remaining HDB mortgage of $200,000.

Focus on Debt Free

A couple who is focused on being debt free will want to use the $200,000 to pay off its HDB mortgage. This is because it essentially means that they are "officially" debt free and as long as they have enough to feed themselves, they will have a roof over their head. This couple wants to "sustain" their lifestyle.

Focus on Cash Flow

A couple who is focused on cash flow will weigh the alternative use of the $200,000. If they can invest the $200,000 in a relatively safe manner (say in a corporate bonds or REITs) yielding 5% p.a., they would effectively have earn an arbitrage difference of 3% (assuming 2% mortgage loan). Hence every month, their $200,000 will earn 200,000 x 3% / 12 = $500 per month. An extra $500 per month! Not too bad actually if they can eventually generate passive income to cover their lifestyle . This couple wants to "maintain" their lifestyle.

Focus on Net Worth

A couple who is focused on growing net worth will actually view it differently. They will put the $200,000 in the "mortgage-one account" to offset the home loan interest (HSBC and SCB offers such loans previously) and wait for opportunities to use that $200,000. When the opportunities arise, they will invest within their area of competence, be it in properties or stocks or other assets. (I have shared with you previously why properties are preferred because of the leveraging effect). This couple is not afraid to take on "good debts" and in a few years, their net worth multiplied because of the good "debts" and increased in value of their stocks and properties. This couple wants to "enjoy" their lifestyle.

What mindset do you have?

I have a friend who is a few years older than me but his original focus was on being debt free. When the opportunities came, he didn't have the "bullets" to pull the trigger as he has just paid off his HDB mortgage loan. You must also remember that banks prefer to lend money to younger couples in their early 30s. As you aged, the ability to borrow from banks actually falls, especially with all the mortgage rules being implemented.

When i was in my early 30s, my focus was on growing my net worth. Now that i have crossed 40, i am beginning to pay slightly more attention on generating stable yields (or passive income) but my priority is still focus on growing my net worth. Once i cross 50s, i will want to ensure that i have stable passive income that will allow me to maintain my lifestyle for the next 20 years (assuming i can live till 70s).

SRS and me

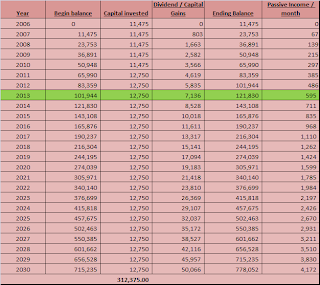

As i reflect back on my SRS account in 2013, i think i am actually too "hung up" on finding yields and creating passive income. I should instead be focused on investing in great businesses and growing my net worth given that i am still relatively young. As such, l would like to change my mindset a bit for the SRS account from 2014 onwards. I would like to take a more balanced approach between finding good dividend-paying stocks as well as growth stocks that will generate the alpha to grow the net worth. The table below shows the portfolio growing at a compounded 7% per annum, i am actually slightly behind for 2013.

My SRS balance is ~$119,873 versus the targeted $121,880. Let's see if i can "catch up" in 2014 to grow it to $143,108 in 2014 with a lofty target of $778k in 2030.... seemed so far away.

SRS and wifey

To help fund our retirement, i have actually seized control of her SRS account as well and in fact, contributed the money there ^_^. I will share with you periodically her account but her focus (given that it is my money and her low risk nature) will probably be in the more boring stocks that pays dividends every year.

2014 - What stocks to invest?

This may surprise you but i am actually currently looking at a China stock that is in the clean environmental space. China has a huge need to clean up its air and water. In fact, there is a news article today on the opportunities. I will post about it if i managed to get in at the price i want.

Happy SRSing and focus on having the right mindset (if you are still young!) :)

I like you using the description of "seize control" of your wife's SRS acct because I also did the same to her CDP/brokerage acct. vested in dividend yielding stocks.

ReplyDeleteDoes seems that our wifey have something in common! Not very interested to invest or abit lazy? Haha. Lucky them have us good husbands that cares!!

Happy new year! Wish u good health and meeting yr investment goals for 2014! Cheers!

Tks for visiting. My goal stretched all the way to year 2028. The seizing control of brokerage accounts happened around the same age as you did :)

ReplyDeleteYou are right to focus on the family as your priority. Once you set your priority right, the rest will just fall in place.

Your wife is smarter than you think la. They know how to choose a good husband to take care of them. Hahaha. Enjoy and have a blessed year ahead.

wow you just put REITs and safe together in one sentence.

ReplyDeleteHaha ok maybe not so safe REITs. I did pause for a while but technically it shouldn't be as volatile as it is a yield product.

DeleteWhy would a couple want to be debt free when they can take on good debts like you said? Even if a couple is conservative I just didnt think paying off the lump sum mortgage is the right way to go.

ReplyDeletePeople have different ideas la, some just like the feeling of having no liability at all. There is a Chinese saying 无债一身轻

Deleteprobably young folks have never been squeezed before and their situation is that they will never be squeezed.

DeleteMay be some folks don't have older relatives or parents who were retrenched during bad times and can't find job for a long time; otherwise their thinking on job security and draw-down for survival may be different.

DeleteOur values are all shaped by life experiences so no one size fixed all for pursuit of financial freedom. Everyone has to walk their own paths :)

ReplyDeleteI didn't actually think of the different mindsets. Was too focused on free cash flow and guess you are right that one should focus on building net worth while they are young. Will start working this this direction. Thanks!

ReplyDeleteEnjoy the journey! :)

DeleteHmm... over $770K in SRS by 2030. You can only withdraw at half-tax rate at statutory retirement age of 62, and you have only 10 years to do full withdrawal => i.e. each year withdraw $70K half-taxable "salary" from your SRS account.

ReplyDeleteIf your SRS investments are too successful (you multi-bag your investment), you might end up paying more in tax later than what you saved now? I suppose that is a happy problem to have.

There is also the problem of whether you want to retire early but your early retirement fund is in your SRS and you can't touch it without the extra 5% tax penalty.

Mutli bag investment. That will be a happy problem. Does SRS take into account whether the gain comes from capital? Currently capital gain don't attract tax.. I better check this with IRAS.

DeleteI enjoyed reading this article, especially the portion on how you would invest $200,000. For me, if I have $200,000, I would not pay off my housing loan. Because the property value rise and fall. So if after paying off the mortgage, the value of my property drop and I need to sell, what I get back might not be the price I paid in full. Furthermore property investment is so illiquid. I would rather use the money to invest in 2nd property.

ReplyDeleteRegards,

Gerald

www.sgwealthbuilder.com

I guess passive income is many times misinterpreted and I think you bring up some good points. Thanks!

ReplyDeleteHi,

ReplyDeleteThanks for sharing this post. Enjoy reading your blog. I haven't started thinking about SRS account because it feels like I am locking up the money for a long time and will lose some flexibility albeit the tax advantages. But will be exploring it in greater detail after reading your post.