SRS Portfolio Update - March 2020

I probably got complacent with the virus . . . in the sense that i saw it coming and could have done something to my portfolio but I didn't, resulting in Frasers Commercial Trust and some SGD bond position turning from a profit into a loss position. For the bonds positions, i am not too worried as the bonds are of investment grade and i will get back my principal at maturity.

One of wifey's position in Aspial Bonds paying 5.3% will be redeemed in April 2020 after 4 years. I first wrote about the bonds here and luckily it wasn't an Hyflux situation. I will probably avoid such bonds going forward.

Massive sell down in markets due to margin calls

The banks have been very generous with providing leverage over the last few years and the last 3 weeks have been a "wake up call" for many of the clients who realised that they are 'screwed' by their own banks. First of all, they sell them so called "safe" products and then provided leverage against them. When the value of these products fell, they asked the clients to top up with cash or the assets will be forced sold.

That is what you have been witnessing in the last 3 weeks.

Takeaway - Don't be overly leveraged. Leverage works both ways. Always keep a safe margin when you gear up.

If you have not been using leverage, you shouldn't worry about margin calls, especially if you invest with the SRS account that can't take leverage. ^_^

What stocks am i looking at?

In my previous post, i mentioned some of the sectors that i am avoiding, so what am i looking at right now?

If you have been hunting for a property for some time and suddenly the value of the property you are looking at drops by half due to poor sentiments, would you buy it?

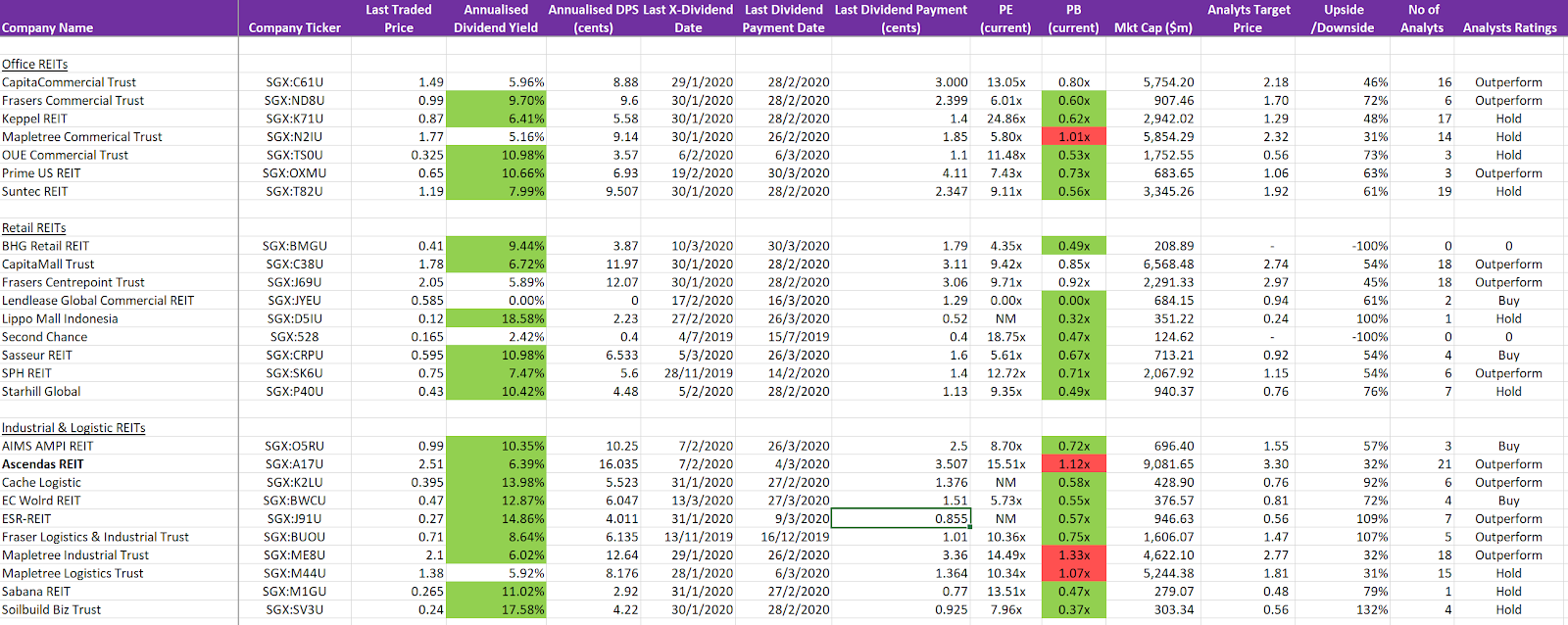

This is what i am doing currently. I have this giant spreadsheet that is updated by Capital IQ and it tracks all the dividend stocks that i am monitoring, including REITs.

I find the REITs sector particularly attractive because (1) they pay regular distributions to maintain their special tax status (2) some are trading at attractive valuations, way below book value (3) unless all the tenants go belly up, the businesses will still need to service the debt, regardless of whether they use the premises or not. Do you stop paying your mortgage because of the crisis?

These are my selection criteria:

- Price to book must be below 1x. The lower the better, indicating "value for money" purchases.

- Properties are managed by reputable sponsors, meaning they will manage the balance sheet and liquidity well.

- Prefers commercial or retail REITs with long WALE. These rentals are recurring in nature. I would avoid hospitality and industrial REITs for now.

- Yield of more than 5%. Many of the REITs are trading above 5% currently even after i imputed a 25% haircut in my DPU assumptions.

A snapshot of my giant spreadsheet is below.

Portfolio Update

I bought into Lendlease, Starhill and Suntec last week but I didn't size my position in Suntec properly. I had wanted to buy on the way down.

My two orders of 50k of Lendlease and 50k of Starhill at lower prices were not filled but i am not too worried.

As of today, i am sitting on unrealised losses of $16k and still have about $102,948 of dry powder in my SRS account.

I will top it up with $15,300 for the current year in April.

The prices may continue to go lower but you will have to "wait it out" as the crisis may worsen.

Happy SRSing !

Comments

Post a Comment